Getting a brand-name medication can feel like a financial punch in the gut. You have insurance, but your copay is $1,200 a month. Then you hear about a copay assistance card-a lifeline that cuts that cost to $0. Sounds perfect, right? But here’s the catch: if you don’t understand how it works, you could be hit with a $2,400 bill in July, even though you paid nothing in January through June.

What Exactly Is a Copay Assistance Card?

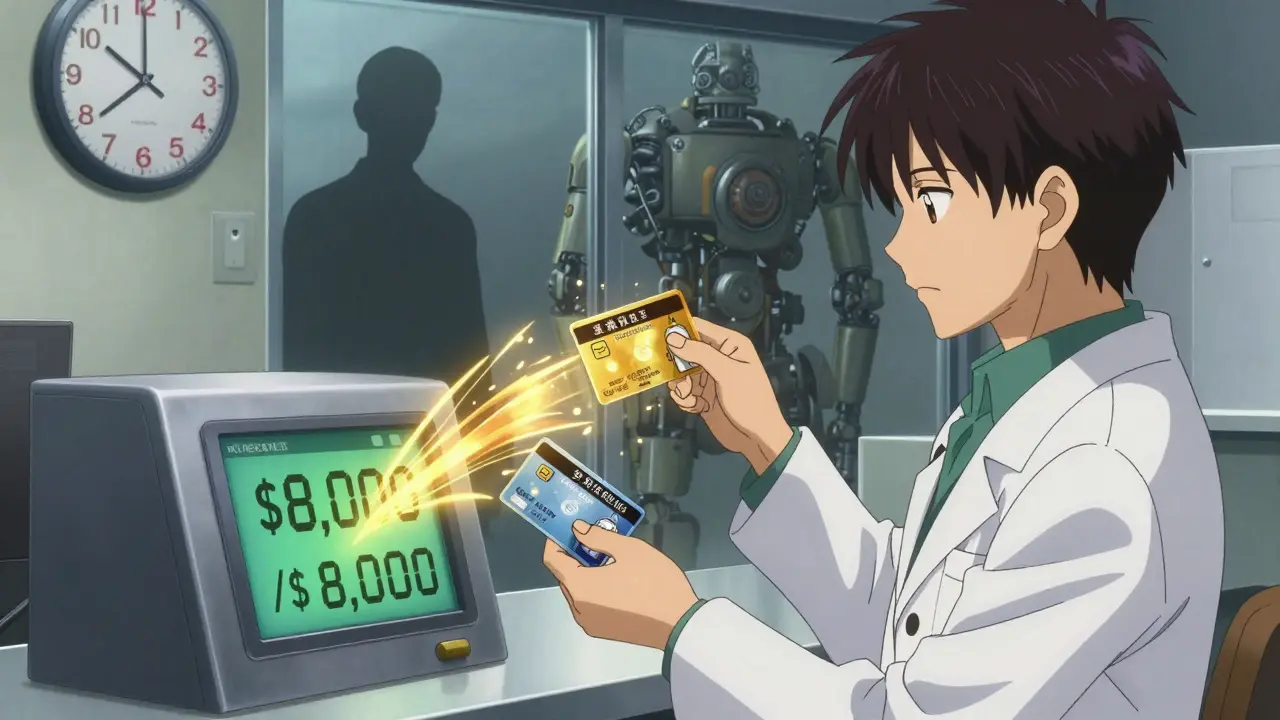

A copay assistance card is a coupon issued directly by the drug manufacturer. It’s not a discount card you buy online. It’s not a government program. It’s a financial tool made by companies like AbbVie, Roche, or Novo Nordisk to help people who have private health insurance pay for expensive brand-name drugs. These cards are mostly used for specialty medications-things like biologics for rheumatoid arthritis, insulin for diabetes, or drugs for multiple sclerosis-that often have no generic version and can cost over $2,000 a month.The card works like this: when you fill your prescription, the pharmacy swipes your insurance card and then your copay card. Your insurance pays part of the cost. The manufacturer pays the rest-up to a set limit. That limit is often $8,000 a year. So if your monthly copay is $2,000, you pay nothing for the first four months. Then? You’re on your own.

Who Can Use These Cards?

You can only use a copay assistance card if you have private, commercial insurance. That means if you’re on Medicare Part D, Medicaid, or if you’re uninsured, you’re not eligible. This is federal law. The government doesn’t allow drug manufacturers to subsidize government programs, so these cards are legally blocked from being used by Medicare beneficiaries.That’s a big deal. Over 60 million Americans are on Medicare. Many of them take expensive medications. They can’t use these cards. Instead, they rely on patient assistance programs run by nonprofits or the manufacturers themselves, which have different rules and income limits. If you’re on Medicare, don’t waste time looking for a copay card for your insulin or rheumatoid arthritis drug-it won’t work.

The Hidden Trap: Copay Accumulator Programs

Here’s where most people get blindsided. Many insurance plans now use something called a copay accumulator program. That means the money the manufacturer pays through your card doesn’t count toward your deductible or your out-of-pocket maximum.Let’s say your plan has a $5,000 deductible. You’ve been using your copay card for six months. You’ve paid $0 out of pocket. But because your plan is an accumulator plan, your deductible is still $5,000. When your card runs out in July, you now have to pay the full $2,000 monthly copay-not just for the rest of the year, but until you hit that $5,000 deductible. That’s $2,000 in July, $2,000 in August, $1,000 in September. Suddenly, you’re out $5,000 in three months.

According to the Kaiser Family Foundation, about 70% of commercial insurance plans in the U.S. now use copay accumulators. That’s not rare. It’s the norm. And most patients don’t know until it’s too late.

Copay Maximizer Programs: The Rare Good News

There’s one exception: copay maximizer programs. These are rare, but they’re the opposite of accumulators. In a maximizer plan, the manufacturer’s contribution is spread evenly across the year to reduce your monthly cost. So if your card gives you $8,000 in assistance and your monthly cost is $2,000, the plan might stretch that $8,000 over four months to cover your copay in full-but then stop. You still pay $0 for those four months. But unlike an accumulator, the $8,000 does count toward your out-of-pocket maximum. So when the card runs out, you’re already halfway to your cap.Maximizer plans are uncommon, but they’re better. If your plan uses one, you’re lucky. But you still need to track your usage. Don’t assume it’ll last the whole year.

How to Get a Copay Assistance Card

Getting one is simple, but you need to do it right.- Go to the drug manufacturer’s website. Search for the exact name of your medication. Look for “Patient Assistance,” “Copay Card,” or “Savings Program.”

- Fill out a short form. You’ll need your insurance info, your doctor’s name, and sometimes proof of income. You don’t need to be under a certain income level-just have private insurance.

- Download the card. Most are digital now. You can save it on your phone or print it out.

- Bring it to the pharmacy every time you refill. Tell the pharmacist you’re using a manufacturer copay card. They’ll process it with your insurance.

Some pharmacies will automatically apply the card if you’re on the right plan. But don’t rely on that. Always ask.

How to Avoid Getting Screwed Over

The biggest mistake people make? Not asking about their plan’s rules before they start using the card.Here’s what you need to do:

- Call your insurance company. Ask: “Does my plan use a copay accumulator or maximizer program for [medication name]?”

- If they say “accumulator,” you’re at risk. Ask: “Will the manufacturer’s payments count toward my deductible or out-of-pocket maximum?” If they say no, you need a backup plan.

- Calculate how long your card will last. Divide the annual limit ($8,000) by your monthly copay ($2,000). That gives you four months. Mark your calendar: four months from now, you’ll owe the full price.

- One month before your card runs out, contact the manufacturer’s patient support line. Ask: “Do you have a bridge program or a transition plan?” Some manufacturers offer extended help for a few months.

- Also, check if you qualify for a nonprofit patient assistance program. Organizations like the Patient Access Network Foundation (PAN) or the HealthWell Foundation can help if you’re under a certain income.

Copay Cards vs. Pharmacy Discount Cards

Don’t confuse copay cards with discount cards like GoodRx or SingleCare. They’re totally different.- Copay cards are from drug makers. Only work with private insurance. Only for brand-name drugs. Can’t be used by Medicare patients.

- Discount cards are from third parties. Work instead of insurance. Can be used for generics or brand-name drugs. No insurance needed. No income limits. No annual cap.

If you’re on Medicare or uninsured, discount cards are your best bet. They often give you lower prices than insurance copays-even with a copay card. For example, a $2,000 insulin pen might cost $1,500 with insurance and a copay card, but only $90 with GoodRx.

But if you have private insurance and need a specialty drug with no generic? The copay card is still your best option-if your plan doesn’t use an accumulator.

What Happens When Your Card Runs Out?

This is the nightmare scenario. You’ve paid $0 for four months. Then, bam-your bill jumps to $2,000. You can’t afford it. You skip doses. Your condition worsens.That’s why timing matters. Don’t wait until your card expires to look for help. Start early.

Call your doctor’s office. Ask if they have samples or can help you apply for a manufacturer’s long-term patient assistance program. These programs often require income verification, but they can cover you for a year or more. Some even cover you if you’re over the income limit-just because you’re on a high-cost drug.

Also, check with your state. California, New York, and a few others have passed laws forcing insurers to count manufacturer payments toward out-of-pocket maximums. If you live in one of those states, you’re protected. If not? You’re on your own.

Final Advice: Know Your Plan, Know Your Card

Copay assistance cards are powerful-but only if you use them wisely. They’re not free money. They’re a temporary bridge. And if you don’t plan for what comes after, that bridge collapses.Here’s your checklist before you even pick up your first prescription:

- Confirm you have private insurance-no Medicare, no Medicaid.

- Find the manufacturer’s card online. Download it.

- Call your insurer. Ask: “Do you use a copay accumulator or maximizer?”

- Calculate how many months your card will last.

- Set a reminder: one month before it runs out, start looking for backup help.

- Ask your doctor about samples or long-term assistance programs.

If you do this, you’ll avoid the worst-case scenario. You’ll keep taking your medication. You won’t be blindsided by a $10,000 bill. And you’ll stay in control.

Can I use a copay assistance card if I’m on Medicare?

No. Federal law prohibits pharmaceutical manufacturers from providing copay assistance to patients enrolled in Medicare Part D, Medicaid, or other government-funded programs. These cards are only for people with private, commercial insurance. If you’re on Medicare, look into nonprofit patient assistance programs or pharmacy discount cards like GoodRx instead.

Do copay cards count toward my deductible?

It depends on your insurance plan. If your plan uses a copay accumulator program, the manufacturer’s payment does NOT count toward your deductible or out-of-pocket maximum. If it uses a copay maximizer program, the payment does count. Most plans (about 70%) are accumulators. Always call your insurer to confirm.

How much money can I save with a copay card?

Most cards offer up to $8,000 in annual savings. If your monthly copay is $2,000, that means you pay $0 for the first four months. After that, you pay the full amount unless your plan is a maximizer or you qualify for other assistance. Some cards cap at $5,000 or $10,000-check the card’s terms.

Can I use a copay card with a generic drug?

No. Copay assistance cards are only for brand-name medications. Manufacturers don’t offer these cards for generics because they don’t need to compete on price. If you’re on a generic, your best option is a pharmacy discount card like GoodRx, which often gives you lower prices than your insurance copay.

What should I do if my copay card runs out and I can’t afford my medication?

Don’t stop taking your medication. Contact the drug manufacturer’s patient support line immediately-they may have a long-term assistance program. Also, reach out to nonprofits like PAN Foundation, HealthWell Foundation, or NeedyMeds. These organizations help people pay for high-cost drugs even if they earn too much for Medicaid. Your doctor’s office may also have samples or connections to financial aid programs.

Lindsey Kidd

December 24, 2025 AT 03:33This made me cry 😭 I’ve been using my insulin card for 6 months and just found out my plan is an accumulator. I thought I was saving money… turns out I’m just building a debt bomb. Thanks for the heads-up, I’m calling my insurer tomorrow.

Rachel Cericola

December 25, 2025 AT 03:20Let me just say this: if you’re on a brand-name drug and have private insurance, you are NOT off the hook just because your copay is $0 right now. The system is designed to make you feel safe until it isn’t. I work in healthcare policy and I’ve seen people lose their homes because they didn’t know about accumulator programs. It’s not a glitch-it’s a feature. Manufacturers get the PR win of ‘helping patients,’ insurers get to shift costs, and patients get blindsided. You need to treat this like a ticking time bomb. Set calendar alerts. Call your insurer. Ask for the exact policy number. Don’t trust the pharmacy. Don’t trust the website. Call. And if you’re on Medicare? GoodRx is your best friend. I’ve seen people pay $90 for insulin instead of $1,200. It’s not magic-it’s just knowing where to look.

CHETAN MANDLECHA

December 25, 2025 AT 04:45Interesting. In India, we don’t have such systems. Medicines are either cheap generics or bought out of pocket. But I see how complex this is in the US. I wonder if this is why so many Americans avoid taking meds even when prescribed. The fear of hidden costs. It’s not just about price-it’s about trust in the system.

Ajay Sangani

December 26, 2025 AT 11:26so… if the manufaturer pays the copay… but it dont count to the max… then who is really paying? the insurance co? but they pay less… so its like… the patient is getting a free ride until the card runs out… but then they owe the full amount… so its not really a subsidy… its a delay… like a loan with no interest but a brutal repayment schedule… i think this is unethical… but also… legal… which makes it worse

Pankaj Chaudhary IPS

December 27, 2025 AT 21:51As someone who has worked with underserved communities across India and the U.S., I can say this: healthcare access should never be a lottery. The fact that a life-saving medication can be rendered inaccessible due to arcane insurance mechanics is a moral failure. Copay assistance cards are not charity-they are a band-aid on a hemorrhage. What we need is systemic reform: price caps, mandatory accumulator bans, and universal access to affordable biologics. Until then, educate yourself, advocate for others, and never assume the system has your back. You must be your own advocate. And if you’re reading this and have privilege-use it to help someone who doesn’t.

Payson Mattes

December 28, 2025 AT 12:17Wait… so you’re telling me the drug companies are using these cards to keep people dependent on their expensive meds? And the insurers are in on it? This is a scam. They want you to get hooked on the drug, then hit you with the bill when the card expires. And the FDA lets this happen? I bet the CEOs are laughing all the way to the bank. I’ve got a friend who got a $14k bill after 5 months of $0 copays. They’re not helping you-they’re manipulating you. And if you’re on Medicare? They don’t even care. This is capitalism at its most predatory.

Steven Mayer

December 28, 2025 AT 19:56The structural asymmetry inherent in the copay assistance mechanism creates a perverse incentive alignment between manufacturers, PBMs, and insurers, wherein the externalization of cost burden onto the insured population is optimized through the deployment of accumulator protocols. The absence of regulatory intervention in this domain constitutes a market failure of epistemological magnitude. Patient outcomes are subordinated to actuarial calculus. The notion of ‘affordability’ becomes a rhetorical artifact rather than a functional reality.

Diana Alime

December 29, 2025 AT 04:33so i just spent 4 months paying $0 for my rheumatoid arthritis drug… and now i have to pay $2k a month until i hit $5k deductible?? i feel like i got catfished by my insurance company 😭 i’m crying in the pharmacy aisle rn

Adarsh Dubey

December 30, 2025 AT 04:19Thank you for this comprehensive breakdown. Many people don’t realize that the term 'copay assistance' is misleading-it implies help, but the reality is conditional and often temporary. The key takeaway is not just to get the card, but to map out the entire financial trajectory of your treatment. Planning ahead isn’t paranoia-it’s survival in today’s healthcare landscape. I hope more people share this knowledge. It’s the kind of information that saves lives.